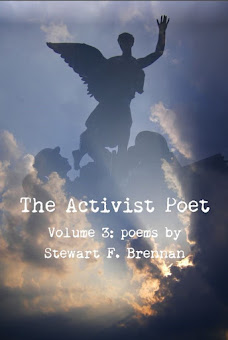

French minister

of Economy, Finances and Foreign Trade Pierre Moscovici (R) and International

Monetary Fund chief Christine Lagarde (L) chat next to EU Commissioner for

Economic and Monetary Affairs Olli Rehn (C) prior to an extraordinary Eurozone

meeting on March 24, 2013 at the EU Headquarters in Brussels (AFP Photo / John

Thys)

Source: Russia Today

http://rt.com/news/cyprus-eu-imf-bailout-764/The Eurogroup has approved a deal on a 10 billion-euro bailout for Cyprus, struck early Monday in Brussels. Cyprus avoids exiting the eurozone, but will have its second largest bank closed with heavy losses expected for big depositors.

“The size of financial assistance will amount to 10 billion euro,” Eurogroup president Jeroen Dijsselbloem has announced at a press conference in Brussels after the eurozone finance ministers swiftly endorsed the plan.

“With this agreement we’ve put an end to the uncertainty that has affected Cyprus and the euro area over the last few days,”he added.

The new deal agreed between Cyprus and the Troika of international lenders - the EU, the ECB and the IMF - will set up a "good bank" and a "bad bank" and will mean that the country’s second largest bank Laiki will effectively be shut down.

Deposits below 100,000 euros will be shifted from Laiki to the Bank of Cyprus to create a “good bank.” Deposits larger than 100,000 euros will be frozen and used to resolve debts. It remains unclear how large the write-down on those funds will be.

The decision comes hours before the Monday deadline set by the European Central Bank, following heated talks between President Nicos Anastasiades and the Troika.

Earlier on Sunday the central bank in Cyprus has imposed an ATM withdrawal limit of 100 euros per day for the island's two biggest banks, in order to prevent a run on lenders.

Warren Pollock - market analyst and financial adviser says the financial turmoil in Cyprus is part of a broader crisis.

“In reality this is a global problem which has not been addressed since 2007-2008 and previous to that with the issuance of huge amounts of debt and leverage into the system both in Europe and in the United States,” he told RT.

“And when that debt goes bad, the only recourse which exists is to tap remaining collateral in the system which is the savings.”

Pollock believes that sooner or later this “sort of stealing” of savings may result in popular unrest. “We can definitely see smaller countries being the test to see whether savings could be stolen on a wider scale.”

a.jpg)

a.jpg)

No comments:

Post a Comment

Thanks for commenting on this post. Please consider sharing it on Facebook or Twitter for a wider discussion.